LAGARDE'S CUT

Why Europe Cannot Win the Stablecoin Race By Trying to Run It

The Cut Lagarde Drew, and the One She Withheld

There is a specific kind of silence that follows when a central bank president says the quiet part out loud. On 8 May 2026, Christine Lagarde broke a two-year European policy taboo.

She wrapped it in the dry, deliberate vocabulary of Frankfurt, but read in plain language, her statement crossed a line the European policy apparatus has spent billions trying to defend:

If we want to strengthen the international appeal of the euro, stablecoins are not an efficient way of doing so.

Read it twice. It is a capitulation on the battlefield of issuance.

In a single public intervention, the President of the ECB drew a distinction that central bankers spend their careers avoiding in public. She separated the stablecoin as an instrument (a digital token, easy to issue and regulate) from the stablecoin as a function (the underlying architecture of global settlement). The instrument is moved by code. The function lives in the plumbing.

It is the exact cut you make when you stop arguing about sovereignty-by-decree and are forced to look at the pipes.

But then she stopped. She had to. The head of the ECB cannot publicly state where her own logic leads, because the conclusion exceeds her mandate. She left the forced mate on the board, expecting the room to see it.

The room, predictably, missed it. They read her gesture as a comfortable defense of a future Digital Euro paired with a policed EUR-stablecoin market. That reading is comfortable. It is also structurally backwards. Lagarde’s cut does not point toward a European stablecoin. It points away from one.

The Stakes for Europe

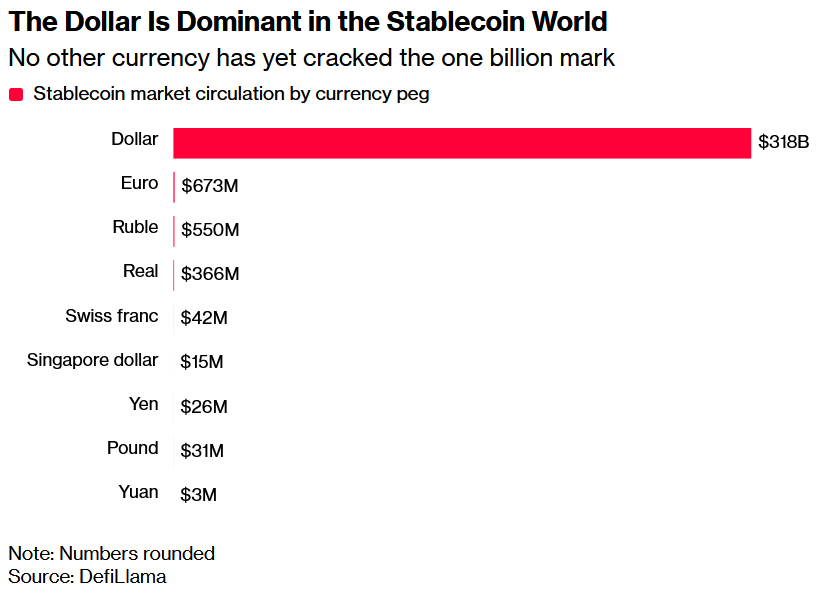

Before the argument, the data. As of 8 May 2026, DefiLlama reports the following circulating stablecoin supply by currency peg:

On the morning of the speech, Nic Puckrin distilled the same data to a single ratio. The dollar-stablecoin market capitalization is roughly 473 times the euro-stablecoin market capitalization. Of every dollar of stablecoin float in circulation, more than 99% is denominated in dollars. Everything else combined, every euro-stablecoin, every rouble-, real-, franc-, pound-, yen-, Singapore-dollar-, and yuan-stablecoin issued anywhere on any chain, fits inside the remaining half of one percent.

That is not a market signal. Markets fluctuate. Half a percent versus ninety-nine and a half percent is not a fluctuation. It is a network state. It tells you that the architecture has already chosen, and that no policy made in Brussels or Frankfurt is going to redistribute that share by decree. You can regulate against it. You can subsidise alternatives. You can pass MiCAR. The gravity does not move.

Europe is therefore not facing a choice between a euro-stablecoin and a dollar-stablecoin. Europe is facing a choice between three positions, and only three:

Accept dollar-stablecoins as the de-facto settlement medium for digital euro flows, and let MiCAR police the edges.

Build a regulated euro-stablecoin market and try to defend share that has not yet been won, against an opponent that already controls the field.

Adopt the layer underneath the stablecoins, which is neutral by construction, and stop fighting an issuance battle that cannot be won on issuer terms.

The first position is surrender disguised as pragmatism. The second is the position the ECB is being pushed toward, and the one that sounds most like sovereignty without being it. The third is the only one that takes Lagarde’s own cut seriously.

Why the Bait Should Not Be Taken

The bait, in this argument, is the temptation to answer the question ‘how should Europe respond to dollar-stablecoin dominance?’ by issuing a competing instrument. The instinct is older than the technology. Every monetary regime under pressure asks the same thing: what does our version look like? And in most cases the answer is to build one and let it lose, because the loss is less embarrassing than the abdication.

The instinct to build a domestic competitor shatters against three structural realities.

1. Liquidity asymmetry is not closeable.

Stablecoins are not just tokens. They are network goods. Their value to a holder rises with the number of other holders, with the number of venues that quote them, with the depth of the market-making book that trades them, and with the number of protocols that accept them as collateral. Each of those numbers compounds. Each of those numbers, today, sits at near-saturation for USDT, USDC and RLUSD and at near-zero for any euro-stablecoin issued anywhere.

An issuer entering this market in 2026 does not start from neutral ground. They start at the bottom of a network-effect curve that rises non-linearly. Even if European regulators force every European exchange and every European bank to integrate a euro-stablecoin first, the global liquidity that stablecoins are actually used for, settlement across jurisdictions, lending into DeFi, payments outside the issuing currency’s home zone, will continue to flow in dollars. The European user gets a token that works at home and stops working the moment value crosses a border. That is not a stablecoin. That is a digital giro account with a token wrapper.

2. The Forced-Buyer trap is lethal in EUR.

As established in ‘Forced Buyer’, the GENIUS Act has turned dollar-stablecoin issuers into structural buyers of US Treasuries. The sovereign gains a captive buyer, suppressing yield. The US tolerates this because it funds their empire.

Replicating this structure in Europe is not sovereignty; it is a macroeconomic suicide pill. Backing a massive regulated EUR-stablecoin means parking reserves in German Bunds, French OATs, and Italian BTPs. The issuer becomes a systemic buyer of European sovereign paper.

The ECB — already trapped by a balance sheet swollen with sovereign debt — gains a new, unmanageable source of structural demand. The yields it wants suppressed get suppressed harder. The moment inflation returns, the ECB loses the freedom to raise interest rates without crashing the value of those underlying bonds, risking an SVB-style insolvency for its own digital peg. Paying for the aesthetic of a token with the freedom to set monetary policy is a trade no central bank should sign.

3. The ruler is broken at the source.

The unit of account itself drifts. The Buffett Indicator at 230 percent is not measuring an equity bubble; it is measuring a numerator that has been pulled by liquidity provision while the denominator has been held back by demographics and productivity. The ruler bends under the weight it is asked to carry.

The implication for stablecoins is direct: a token pegged 1:1 to a drifting fiat unit inherits the drift exactly. Nominal balance constant, real balance not. Pegging to a euro that is itself a bending ruler does not stabilize anything; it preserves the drift faster, on better rails. The peg solves a settlement problem, in that you can move euros faster on chain. It does not solve the unit-of-account problem Lagarde herself raised.

The singleness of money, in the strong sense, is not the singleness of an issuer. It is the question of whether the unit you are measuring with means the same thing across time. A euro-stablecoin makes the euro faster. It does not make the euro a better ruler. The two questions are different.

These three reasons are not arguments against having euros on chain. They are arguments against believing that ‘euros on chain’ answers the question Lagarde was asking.

The Cut Lagarde Could Not Make

What is the cut she could not finish?

It is the move from defending the function (a single, trustworthy unit of account for European transactions) to identifying the architecture that actually defends it. That architecture is not an issuer. It is a settlement layer. And the property that makes a settlement layer fit for the purpose Lagarde described is the property she cannot recommend by name: it has to be neutral, in the strong sense. It cannot be owned by any of the issuers it settles for.

Neutrality, here, is not an aesthetic claim. It is structural. A settlement layer issued by one of the participants, or governed by one of their regulators, becomes a chokepoint. It can be censored. It can be tilted. It can be turned into a political instrument the moment the incentives shift. A settlement layer that no participant owns, and that no single regulator controls, is the only configuration in which ‘singleness of money’ actually holds across issuers without collapsing into the dominance of one issuer.

Consider the aqueducts of the Roman Empire. They did not belong to a single province. They moved water across territories that were politically distinct, technologically uneven, and economically competitive. They worked because they were shared infrastructure, maintained by a layer of governance that none of the local actors fully owned. The aqueducts won not by choosing a side, but by making side-choosing unnecessary for the thing they delivered.

A neutral settlement layer for stablecoins, regardless of currency of denomination, is the monetary aqueduct. It does not compete with the euro, the dollar, the yen, or the franc. It lets each of them move, and lets the holder of each redeem, exchange, or pass through without depending on the goodwill of the others. The instrument stays national. The function becomes shared.

This is also where Pontes — the Eurosystem’s wholesale DLT settlement layer launching Q3 2026 — sits structurally. The name promises bridges. Bridges they are, in the literal sense: bridges between TARGET-side wholesale and DLT-side wholesale, both inside the European banking system, both governed by European institutions, both denominated in euros. Bridges between rooms in the same house. They do real work. They do not do the work Lagarde named.

For singleness of money across cross-border, cross-currency, cross-jurisdiction transactions, internal connections are not enough. Pontes will let German, French, and Italian wholesale DLT participants settle in tokenised euros against TARGET. It will not let an French importer settle a real-denominated invoice with a Brazilian exporter without choosing whose plumbing to use. That kind of settlement does not happen on a bridge between European rooms. It happens on infrastructure that does not belong to any of the territories crossed.

Pontes does not need to be replaced; it needs to be recognized for what it is: domestic piping.

The Eurosystem’s own 2024 wholesale DLT trials map this reality perfectly: dozens of banks testing settlement across private EVM, Hyperledger, XRPL Forks and Corda sandboxes. It is brilliant internal engineering to build walled gardens, but isolated laboratory networks do not capture global liquidity.

The implication is that Pontes is necessary and insufficient. Europe needs an endpoint inside the EU through which European participants can reach a settlement layer that no jurisdiction owns. Pontes builds the European house’s internal connections. The window in the outer wall — opening onto infrastructure that crosses territories without belonging to any of them — is the unfinished work. The currency stays European. The internal plumbing is Pontes. The aqueduct is something else.

This is the move the ECB cannot officially recommend, because recommending a specific settlement infrastructure would exceed its mandate and signal preferential treatment of one technology over another. The cut must therefore be finished from the outside.

What the cut requires, once finished, is architecture over narrative. The narrative answer to dollar-stablecoin dominance is to issue a euro-stablecoin and announce sovereignty. The architectural answer is to identify the part of the stack where issuance does not decide the outcome, and to occupy that part. The narrative answer is louder. The architectural answer is the one that holds.

The Trojan in the Architecture

The theoretical argument is over; the data has hardened into structure. Dollar-stablecoins have not just won the issuance war; they have set the strategic terms of surrender for every other monetary actor.

The GENIUS Act has formalized the loop between issuer reserves and US Treasury demand. But the true battle has already moved one layer down. Consider the structural positioning of RLUSD, Ripple’s own dollar-stablecoin. It is a Trojan built inside the dollar-architecture: a highly credible US issuer deliberately pulling volume onto a settlement layer it did not design to be explicitly American.

This exposes the central paradox of the stablecoin war: whoever wins the issuance race (the dollar) cannot be allowed to control the layer underneath it, because that layer must clear for everyone globally. The settlement layer, by virtue of having to be globally trusted, becomes the neutral chokepoint of last resort. Whoever runs that layer — or whoever ensures it is run by no one in particular — controls the only part of the stack the dollar’s network effect cannot capture.

Lagarde just made the European case for this exact architecture, constrained only by her mandate. She named the function. She named the threat. She simply could not name the plumbing.

The neutral layer is not a theoretical construct; the race to provide it is live. Whether that global architecture ultimately hardens around a public EVM environment, a purpose-built neutral ledger, or a yet-to-be-scaled consensus protocol, the European mandate remains identical: aggressive adoption, integration, and governance at the validator level, not petulant token competition. The currency stays European. The settlement becomes shared. That is the inversion Lagarde gestured at, fully realized.

The Brussels Illusions

Any argument against domestic issuance faces immediate pushback from the European institutional consensus. That defense rests on three structural illusions.

Illusion 1: MiCAR is a moat.

The consensus assumes MiCAR governs global liquidity. It does not. It governs jurisdictional surface. A European user can be required to redeem through a regulated venue. The cross-border value that stablecoins actually carry — settlement of trade flows, dollarization of emerging-market savings, use as the unit of account in DeFi protocols — happens outside European supervision. Regulation shapes the European corner of the market. It cannot shift the centre of gravity. A MiCAR-compliant euro-stablecoin is, at best, a domestic product. The relevant competition was always for the global one.

Illusion 2: Plurality equals sovereignty.

The consensus assumes a credible euro-denominated digital alternative is a benefit even if it does not dominate, and that choice is itself a public good. Plurality is fine for consumer welfare. It is not a sovereignty argument. If a euro-stablecoin exists but is not used at scale, European monetary sovereignty rests on the mass of users who voted with their balances for the dollar-stablecoin. The plurality argument concedes the structural battle in advance and asks only for a token-shaped consolation. It is incompatible with the singleness — not the plurality — of money.

Illusion 3: Neutrality is a fiction.

The consensus assumes 'neutral layer' is rhetorical. Validators have jurisdictions. Operators have nationalities. Foundations are based somewhere. The supposed neutrality dissolves the moment a sufficiently powerful actor decides to stop respecting it. The argument has surface plausibility. It collapses on the structural question. Governance distribution is a spectrum, not a binary. A settlement layer whose validator set is jurisdictionally diverse, whose consensus does not depend on any single regulator's enforcement, and whose codebase is open enough to fork is operationally more neutral than a settlement layer issued by one central bank or one regulated bank consortium. Neutrality is not the absence of jurisdiction. It is the absence of a single jurisdictional chokepoint. The XRP Ledger's UNLA mature public network's validator diversity, the ability of any participant to publish a competing UNLnode list, and the practical cost of capturing the network-system are concrete measures of how close the system infrastructure gets to the strong neutrality the argument requires. Imperfect is not fictitious. The strategic question is which available layer is most neutral today, and what European policy should do to keep it that way tomorrow.

All three illusions share a structure: they trade structural sovereignty for surface optics. The neutrality of any settlement layer is a property to be defended, not assumed. European participation in the governance of a neutral layer is itself a way of preserving the neutrality. Adopting the layer does not mean leaving it alone. It means showing up.

Falsifiability

The argument above breaks if any of the following materialize.

A regulated euro-stablecoin reaches sustained share above 5 percent of global stablecoin float by Q4 2027 without regulatory subsidy. Network-effect asymmetry would have to be more closeable than this essay assumes.

Pontes, the Eurosystem’s wholesale DLT settlement layer launching Q3 2026, succeeds in attracting non-EU stablecoin issuers to settle euro-leg flows on it. A central-bank-money settlement anchor would then be performing the neutral-layer work this essay argues only a non-issuer-owned layer can perform.

The prevailing neutral settlement candidate is captured by a single jurisdiction. Consensus diversity collapses, validator concentration crosses a regulatory single-point-of-failure threshold. The neutrality property would be empirically refuted, and the recommendation would have no remaining target.

The ECB issues a formal opinion endorsing a euro-stablecoin issuer mandate by Q2 2027. The Lagarde framing would then have been a transitional rhetorical position, not a structural cut, and the architectural reading offered here would be wrong about its meaning.

Each of these is observable. The thesis is testable.

Closing

Lagarde drew a cut that goes deeper than she is politically permitted to follow. The instrument is not the function. Issuing a euro-stablecoin is the comfortable answer to the wrong question. It provides the aesthetic of sovereignty, but it is merely motion.

The architecture has already moved beyond issuer competition. Europe’s true choice is no longer which currency to put on-chain. It is whether to integrate into the neutral layer that actually settles global flows, or to spend the next decade dying of thirst while admiring our own internal plumbing.

Europe’s monetary sovereignty will not survive by issuing one more compliant peg. It survives by securing a seat at the governance table of the aqueduct that no one issues.

- J.

External video version

A take on the architecture argument. Built independently by William Lolli

Sources

Lagarde, Christine — President, European Central Bank. Public intervention, 8 May 2026. Quoted passage on the international appeal of the euro and stablecoins is taken from that intervention.

Stablecoin supply by currency peg, 8 May 2026 — DefiLlama, /stablecoins. Dollar-to-euro circulating-supply ratio (approximately 473 to 1) computed from the same snapshot.

Eurosystem — Appia / Pontes consultation paper, ECB, March 2026 (ecb.europa.eu/paym), and ECB press release of 11 March 2026. The ‘singleness of money’ vocabulary is drawn from this corpus and from the 8 May intervention.

European Central Bank — The Eurosystem’s exploratory work on new technologies for wholesale central bank money settlement (Annex II), 2024.

Companion pieces

Janus runs 1:1 Confrontation — sixty minutes, one decision, no follow-up. For people who carry responsibility and want their thinking taken apart before it costs them.

janusthewatcher.substack.com/p/11-confrontation

One sentence is enough.