Your Parents’ Wealth Playbook Will Make You Poor

The Cantillon Trap, the End of the Tailwind, and Why the Next Generation Must Build Its Own Engine

“Those who cannot remember the past are condemned to repeat it.”

— George Santayana

“Those who can remember it are condemned to watch everyone else repeat it.”

— The rest of us

Welcome to The Duration Thesis - Essay 1 of 7

How Your Parents Got Rich

Let’s state a macro truth that will deeply offend your financial advisor: your parents’ house was not a brilliant investment. It was a forty-year short position on interest rates. They did not compound wealth through discipline. They surfed the largest, longest monetary easing cycle in the history of fiat currency.

Here is how it looked from the inside. They bought a house in 1995 for $150,000 at 7.5% interest. It felt expensive. Their parents told them they were overpaying. The monthly payments consumed nearly a third of their take-home income, and for the first decade, most of that money went straight to the bank as interest. They were not building wealth. They were renting money.

Then something happened that they did not plan, did not predict, and did not cause: interest rates fell. Not once, but systematically, relentlessly, for the next twenty-five years. They refinanced in 2003 at 5.2%. Again in 2012 at 3.4%. Again in 2020 at 2.6%. Each time, their monthly payment shrank or their equity grew faster. The house, meanwhile, rode the same monetary tide upward. By 2024, it was worth $580,000. They felt like geniuses.

They were passengers.

What happened to your parents was not the result of financial acumen, superior asset selection, or disciplined saving. It was the result of the single most important macroeconomic event of the past half-century: a forty-year secular decline in interest rates, from Paul Volcker’s 20% federal funds rate in 1981 to the zero bound in 2020. This decline was the tide that lifted all leveraged boats. Stocks, real estate, private equity, venture capital — anything funded by borrowed money appreciated in nominal terms as the cost of that money fell toward zero.

This was not investing. It was monetary surfing. And the wave has broken.

The psychologists Daniel Kahneman and Amos Tversky spent decades studying how humans systematically misjudge probability and causation. One of their most powerful findings is survivorship bias: we construct narratives from the winners and ignore the losers. The millions who did not buy property, who bought at the wrong time, who lost their homes in 2008, who were priced out by 2015 — they are invisible. What remains is a curated generational myth: real estate always goes up. Leverage is how smart people build wealth. Your home is your best investment.

None of these statements are laws of nature. They are artifacts of a specific monetary era that is now ending.

The Cantillon Trap

The wealth transfer was not accidental. It has a name and a mechanism.

I have written elsewhere about this architecture in detail — what I call the Temporal Cantillon Effect: the systematic extraction of economic capacity from future cohorts by present ones, operating through credit creation, sovereign debt, pension leverage, and asset inflation simultaneously. The full topology is mapped in a separate essay. Here, the diagnosis is sufficient.

The numbers tell the story without embellishment. In the United States, the median home price relative to median household income was approximately 3.5x in 1980. By 2024, it exceeded 7.5x. Wages, adjusted for inflation, have barely moved. Asset prices, fueled by four decades of falling rates and expanding credit, have roughly doubled relative to the incomes needed to purchase them. The gap between these two lines — wage growth and asset price growth — is the Cantillon dividend. And it has already been paid. To the previous generation.

The generation that borrowed first in the declining-rate environment captured the bulk of the value. They bought assets at pre-expansion prices, with debt that became cheaper to service as rates fell. Each subsequent generation arrived further down the chain: higher prices, tighter margins, thinner upside. The early entrants rode a forty-year monetary wave. The late entrants inherit the undertow.

What macroeconomists call the Long-Term Debt Cycle — a roughly 75-year arc of credit expansion and contraction — explains the rest. The principle is ruthlessly simple: what worked in the last paradigm is precisely what will not work in the next one. The early stages of the cycle reward borrowers. The late stages punish them. The assets purchased at peak leverage become anchors rather than sails.

If you are being told to borrow heavily, buy illiquid assets, and hold for thirty years — you are being handed a playbook from the end of a cycle and asked to run it as if the cycle were just beginning.

In financial markets, when early investors want to cash out massive gains at the top of a cycle, they need someone to buy their bags. In trading, this is called ‘exit liquidity.’ When your parents, the media, and your mortgage broker tell you to stretch your budget to buy a home at 7% interest today, they are not passing down generational wisdom. Mathematically speaking, they are grooming you to be their exit liquidity.

The Temporal Cantillon Effect does not just extract wealth from future generations. As I argue in the full analysis, it extracts the unborn themselves — collapsing fertility rates are not a lifestyle preference but a biological strike against a financially strip-mined future. The system is running out of future to borrow from.

The pitch to “just do what your parents did” is structurally identical to entering a trade at maturity and expecting the same returns as those who entered at inception. It is not financial advice. It is a Cantillon trap.

What They’re Really Selling You

Zoom out from the specific products — the mortgage, the savings plan, the thirty-year fixed, the government-subsidized building society scheme — and examine what the traditional financial stack is actually offering. Every product in this ecosystem shares the same structural DNA:

Illiquidity dressed as “commitment.” Leverage dressed as “smart money.” Duration risk dressed as “long-term thinking.” Intermediary dependency dressed as “expert guidance.”

That word — duration — deserves attention. In bond markets, duration measures how sensitive a position is to interest rate changes. The longer the duration, the more exposed you are. A thirty-year mortgage is one of the longest-duration instruments a retail consumer can hold. The bank does not carry that duration risk. You do. When they sell you “long-term discipline,” they are actually selling you their duration exposure. Your thirty-year commitment is their risk transfer. Your loyalty is their hedge.

There is a pattern that repeats across centuries of institutional design: those who control the rules of a game always design it to reward compliance and punish independence. The financial industry does not need you to be wealthy. It needs you to be predictable. A thirty-year mortgage is not a vehicle for your prosperity — it is a vehicle for theirs. The bank earns interest for three decades. The insurance company earns premiums. The broker earns commission. The tax authority earns revenue on every transaction. Your commitment is their asset. The more years you pledge, the more valuable you become to every intermediary in the chain — and the less optionality you retain for yourself.

There is a question that no mortgage advisor, no building society brochure, and no financial planning seminar will ever ask you: What are the opportunity costs of locking your capital into a non-yielding, illiquid, maintenance-intensive asset for twenty-five years?

A house does not compound. It sits there, depreciating physically, while its nominal price floats on the monetary tide. You pay for the privilege of maintaining it, insuring it, taxing it, and repairing it. After all costs — mortgage interest, insurance, maintenance, property tax, transaction fees — the real return on owner-occupied residential property in most Western markets has been between 0% and 2% annually over the past century. The apparent “gains” were mostly inflation, recycled back to you as nominal appreciation while the currency in which those gains are measured lost purchasing power.

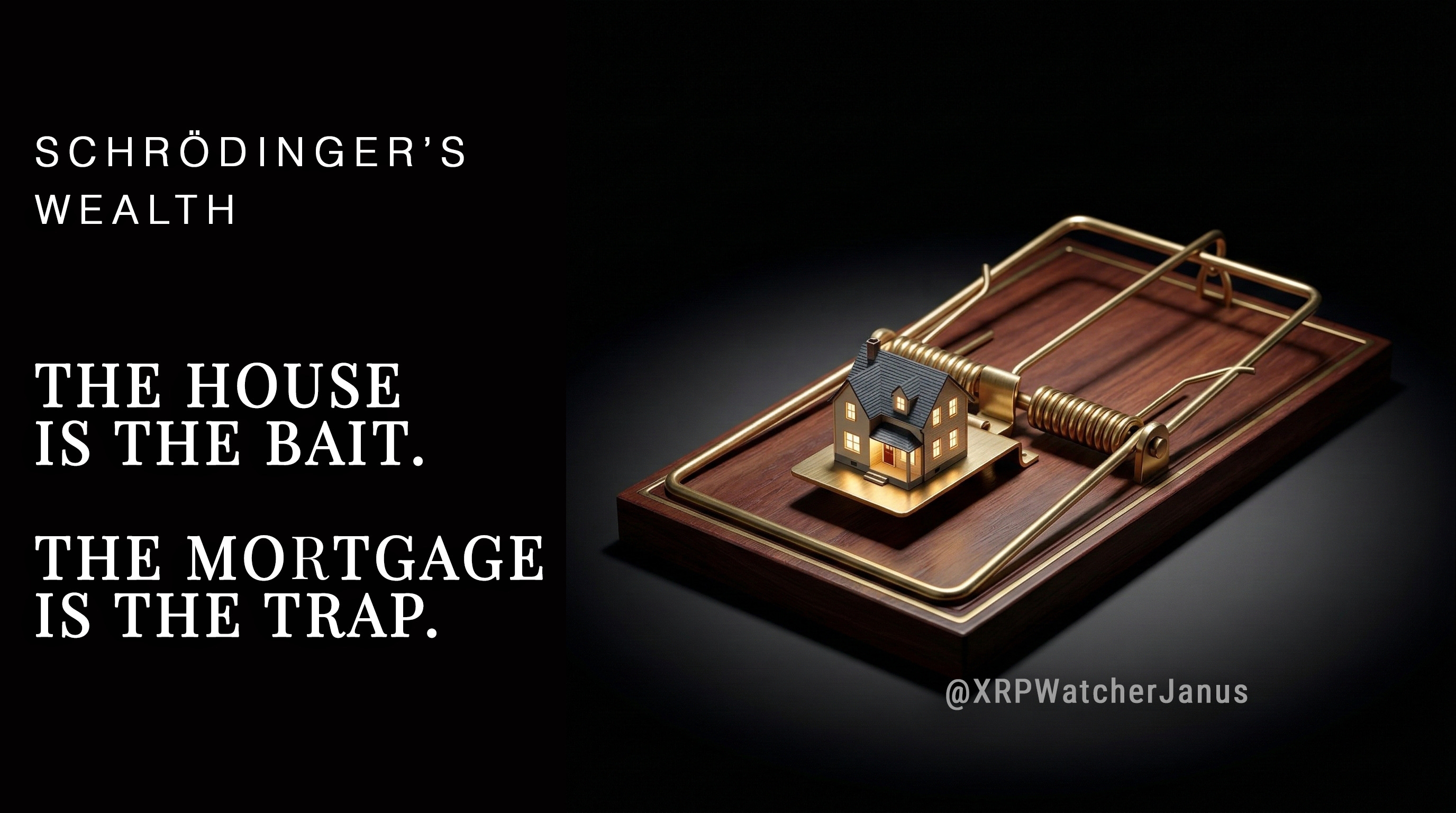

The Double Illusion. Here is the cruelest sleight of hand in the entire architecture. The system sold two promises simultaneously: your house is your home — the place where you live, raise your children, grow old in peace — and your house is your wealth — the asset that appreciates, the retirement fund, the inheritance you leave behind.

These two promises are structurally incompatible. If you live in the house until you die, you never realize the wealth. The only way to extract the “value” is to sell — which means losing the home. Or to take a reverse mortgage — which means giving the home back to the bank in slow motion, the same institution that sold you the dream of ownership in the first place. You end where you began: paying rent, except now to your own equity.

For decades, this contradiction was invisible because rising prices made it feel like both promises were true at the same time. The house went up in value on paper. You lived in it comfortably. The illusion held. But the value was never simultaneously accessible and inhabitable. It was Schrödinger’s wealth — alive as a retirement plan and dead as a home, collapsing into one state only when you tried to use it.

The generation that bought in 1985 could believe both stories because the monetary environment made the contradiction invisible. The generation buying in 2026 cannot afford that luxury. At 7% interest, with a price-to-income ratio above 7x, the math forces a choice: it is shelter, or it is an investment. It cannot be both. And the moment you acknowledge that, the entire narrative architecture of middle-class wealth building — the one your parents handed you as a birthright — collapses into what it always was: temporal extraction, fueled by a financial architecture that monetized both ends of the illusion while you sat in the middle, paying.

The strongest counterargument deserves respect. The best case for the mortgage-property model is not financial — it is psychological. Illiquidity forces savings. Most people, left to their own devices, will consume rather than invest. The mortgage is a commitment device: it binds you to the mast, like Odysseus, forcing wealth accumulation through involuntary discipline.

This is real. It works. Behavioral economics confirms it: humans are catastrophically bad at deferred gratification, and any mechanism that automates long-term saving produces better outcomes than relying on willpower alone.

But binding yourself to the mast is a brilliant strategy only if the ship is sailing toward safety. Odysseus tied himself down because the ship was heading past the Sirens, not toward them. If the ship is heading into a storm — if rates are rising, if wages are stagnant, if the price-to-income ratio makes the bet asymmetrically unfavorable — then the rope that saved Odysseus becomes the anchor that drowns you. Forced savings into a deteriorating structure is not discipline. It is captivity with a thirty-year sentence.

The Inversion

If the old formula is broken, what would a structurally sound alternative look like? Not a product. Not a pitch. A set of first principles — the financial physics of what a wealth-building engine needs to do in a post-tailwind world.

Liquidity. You can adjust your position as conditions change. No six-month escrow, no agent, no paperwork. The ability to move is not a luxury — it is a survival trait in a regime where the rules shift faster than a thirty-year plan can accommodate.

Native yield. The asset generates cash flow not from finding a greater fool to buy it at a higher price, but from performing an economic function. Compensation for a service rendered, not for speculation. Returns that exist independent of monetary policy, independent of the next buyer’s willingness to overpay.

Self-custody. No intermediary holds your asset. No institution can freeze it, deny access to it, or restructure its terms based on a policy change, a credit score, or a political decision. Ownership means ownership — not a claim on someone else’s balance sheet that they can renegotiate.

Programmable duration. You choose your time horizon and adjust as conditions change. Thirty days, ninety days, one year, ten years. No penalty for early exit. No lock-in by design. Duration as a tool you wield, not a cage someone builds around you.

Zero maintenance cost. The asset does not need a roof, a furnace, insurance, or property tax. It does not physically deteriorate while you hold it.

These are not utopian fantasies. They are design specifications. And the question for this generation is not whether such assets could theoretically exist — it is whether you would recognize them if they did. Because the psychological machinery that Kahneman and Tversky mapped — anchoring, status quo bias, loss aversion — does not just affect how you evaluate risk. It affects how you perceive entire categories of possibility. If your mental model of “wealth building” is anchored to a house with a mortgage, then anything that does not look like a house with a mortgage will feel like speculation, even if the underlying mathematics are more conservative.

The distinction becomes clearer through the lens of payoff structure. A leveraged real estate position is a concave bet: limited upside in real terms, catastrophic downside when job loss meets rate increases meets illiquidity. The alternative — liquid, yield-generating, self-custodied — is a convex position: the downside is capped because you retain agency and exit at all times, while the upside remains open through compounding. The principle is simple: seek structures where you benefit from disorder rather than being destroyed by it. The leveraged homeowner is fragile. The liquid yield-holder is, at minimum, robust — and at best, antifragile.

The Devil’s Advocate.

“But it’s volatile!” — So was real estate in 2008. The difference is that you can exit a liquid position in sixty seconds. Try selling a house in a crashing market. Volatility is not risk. Volatility combined with illiquidity is risk.

“But yields could go to zero!” — So can rental income, employment income, and bond coupons. The question is not “is yield guaranteed?” — nothing is. The question is: where is the risk-adjusted return more favorable, and where do you retain more control?

“But it’s not tangible. I can’t touch it.” — Neither is a mortgage-backed security, a government bond, or a dollar bill. Value is consensus, not physicality. A deed to a house is a record in a government database. The question is not whether you can touch the asset. The question is whether the institution that validates your claim can change the rules on you — and what options you retain when it does.

The Generational Reframe

Every generation gets told to follow the playbook of the one before it. And every generation that does arrives too late.

The Boomers’ parents — the Silent Generation and the Greatest Generation — told their children to save cash, buy government bonds, and keep their money in the bank. That advice made sense in the world they knew: a world of stable currencies, modest inflation, and guaranteed government pensions. The Boomers ignored them. They bought stocks and real estate with leverage. And they won — not because they were smarter, but because the monetary environment shifted in their favor in ways their parents’ playbook could not capture.

Now the Boomers tell their children: buy property, take a mortgage, commit for thirty years. It is the same structural advice their own parents gave them — repackaged for a different asset class but carrying the same fatal assumption: that the monetary environment which made it work will persist.

It will not persist. Mortgage rates in the United States are at 6.5–7%. In Europe, 3.5–4% and rising. The forty-year tailwind of declining rates has not just stalled — it has reversed. Government debt levels across the developed world are at historic highs. Fiscal expansion — from defense spending to infrastructure to aging populations — will compete with private borrowers for capital. The cost of money is going up, not down. And with it, the entire leveraged-asset playbook begins to fracture.

Every economic system is, at its foundation, a shared fiction — a story that a sufficient number of people agree to believe. The mortgage-property-retirement pipeline was the dominant financial fiction for seventy years. It is not the only possible fiction. And the transitions between fictions are where the greatest dislocations — and the greatest opportunities — occur. We are in such a transition now.

The most dangerous form of conformity is not the kind imposed by force. It is the kind adopted voluntarily — the kind where people stop thinking and simply repeat what has always been done. The unexamined financial life is the most expensive one. The obligation of each generation is not to inherit assumptions, but to interrogate them — not out of rebellion, but out of responsibility.

The pattern across history is consistent: generational wealth is built by those who recognize the next infrastructure of value, not by those who replay the last one. The question is not “what did my parents do?” The question is: where is the structural tailwind now — behind me, or in front of me?

Build Your Own Engine

There is no universal playbook. Anyone who offers you one is selling something. But there are principles that survive across monetary regimes, across generations, across the rise and fall of shared fictions:

Own assets that generate yield without leverage. If your return depends on borrowed money, your fate depends on the lender.

Maintain liquidity and optionality at all times. The ability to move is worth more than the promise of stability. Stability is what intermediaries sell you in exchange for your freedom.

Never outsource custody of your future to an intermediary. If someone else holds the keys, it is not your asset — it is their liability to you. And liabilities can be restructured.

Understand duration as a weapon, not a virtue. Time is the asset — do not sell it to a bank for the privilege of calling yourself an owner. Duration should be your instrument, not your sentence.

Compound patiently. The greatest returns in history have come not from leverage or speculation, but from patient compounding in the right structure during the right paradigm.

Your parents didn’t have a strategy.

They had a tailwind. The tailwind has turned.

Build your own engine — or become exit liquidity for those who did.

So where does that leave us? If the traditional financial architecture is a forty-year tailwind that has reversed, and its products are duration traps dressed as discipline — where do we look? The answer should be obvious: a financial system built on liquidity, native yield, self-custody, and programmable duration already exists. It is called decentralized finance.

But there is a problem. A serious one.

If you step outside the old system and look at the new one, you will not find a solution. You will find a casino. A hyperactive, memoryless, ninety-day sprint machine that has built all the right tools — and forgotten the single most important concept in all of finance: time.

That is the subject of the next essay.

- J.

Author’s Note

My first book “The Proto-Postnational Age” covers the structural forces behind this thesis — why redistribution fails and ownership through protocols is the path forward.

My second book, “The Frame”, just dropped on March 1st. It goes deeper into how consensus systems, ledger theology, and the unbundling of the self reshape what we think of as governance, identity, and value. If this essay resonated, my books are the next level.

This essay contains no investment advice and names no specific assets. The structural argument is the point.