DEFI SOLVED ACCESS AND KILLED TIME.

The 90-Day Casino, Mercenary Capital, and the Most Important Instrument That Doesn’t Exist

“The market can stay irrational longer than you can stay solvent.”

— attributed to Keynes

“The DeFi market can stay amnesic longer than you can stay patient.”

— Observation from the field

Welcome to The Duration Thesis - Essay 2 of 7

The Casino

In the previous essay “Your Parents’ Wealth Playbook Will Make You Poor”, I diagnosed the traditional financial system as a forty-year tailwind that has reversed. Its products — mortgages, savings plans, pension vehicles — are duration traps dressed as discipline, designed to transfer risk from institutions to individuals while monetizing compliance. The playbook that made your parents wealthy will make you poor, because the monetary environment that powered it no longer exists.

The logical next step is to look elsewhere. And elsewhere exists. A parallel financial system, built on open protocols, running twenty-four hours a day, accessible to anyone with an internet connection. No gatekeepers. No credit checks. No thirty-year lock-ins. Native yield. Self-custody. Programmable duration. Every design specification from Essay #1 — met, in theory, by decentralized finance.

In theory.

Because when you actually step inside this system, you do not find a solution. You find a casino. A hyperactive, memoryless, ninety-day sprint machine where liquidity arrives in minutes and disappears in minutes, where capital has no loyalty and no memory, and where the most important concept in all of finance — time — has been structurally amputated.

DeFi solved the wrong problem. It solved access, custody, and intermediary dependency. These are real achievements. But it did not solve duration. And without duration, everything else is noise on a short enough timeline.

The Missing Instrument

Here is a thought experiment that will reframe everything you think you know about decentralized finance.

Imagine the bond market had only 90-day paper.

No 2-year notes. No 10-year treasuries. No 30-year bonds. Just rolling three-month instruments, expiring and resetting every quarter. What would that world look like?

There would be no yield curve. The yield curve — the graph that maps interest rates across different maturities — is the single most important macro indicator in traditional finance. It tells you what the market collectively believes about the future: whether growth is expected or feared, whether inflation is priced in or priced out, whether risk appetite extends beyond the next quarter. Central banks watch it. Treasury departments manage to it. Pension funds build their entire liability structure around it.

Without a yield curve, none of this is possible. There is no price discovery beyond three months. No hedging against rate changes over meaningful timeframes. No calendar spreads, no duration trades, no forward rate agreements. The entire architecture of risk management — the infrastructure that allows institutional capital to operate with conviction across time — simply does not exist.

What you would have instead is a market of sprinters. Every participant optimizing the same ninety-day window. Every strategy converging on the same short-term horizon. Competition would be brutal and commoditized, because without the time dimension, the only variable left to compete on is speed. Who can enter fastest. Who can extract fastest. Who can exit fastest.

This is not a thought experiment. This is a precise description of decentralized finance as it exists today.

The dominant yield products in DeFi operate on horizons of thirty to ninety days. Liquidity pools reset. Incentive programs expire. Yield farms rotate. The market’s collective memory extends approximately one quarter into the future — and forgets everything behind it. There is no instrument that allows a participant to express a view on rates six months from now, one year from now, five years from now. The time dimension has been collapsed into a perpetual present.

In traditional finance, the difference between a 3-month T-bill and a 10-year Treasury is not just a longer holding period. It is an entirely different asset class with different buyers, different risk profiles, different use cases, and different information content. The spread between them tells you more about the state of the economy than any single data point. When the curve inverts — when short-term rates exceed long-term rates — it has predicted every major recession in the past fifty years.

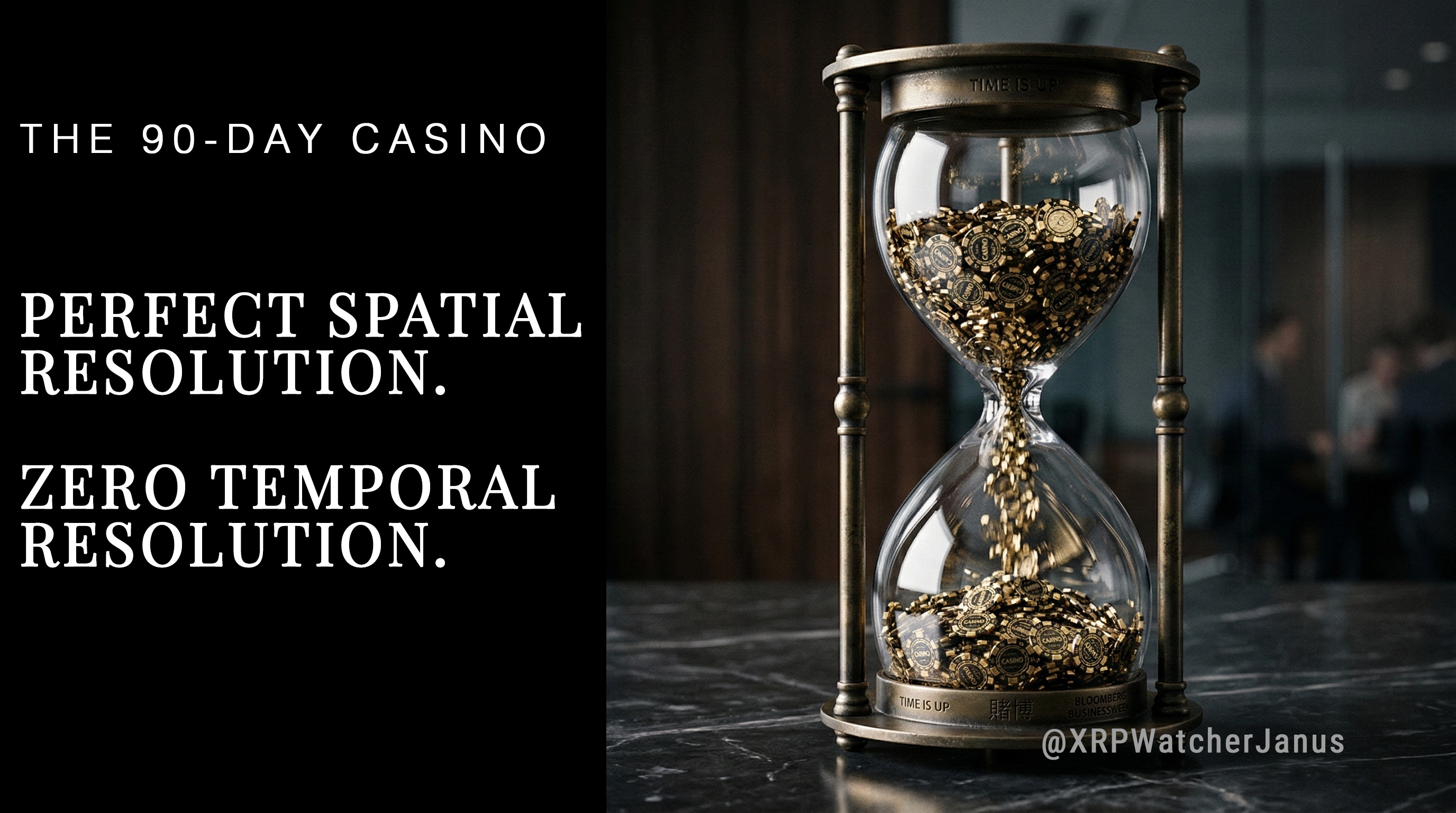

DeFi has no equivalent. It cannot signal what it thinks about the future, because it has no instruments that extend into the future. It is a financial system with perfect spatial resolution and zero temporal resolution. It can tell you exactly what is happening right now, on every chain, in every pool, with every token. It cannot tell you what any of it will look like next quarter. Not because the information is hidden — but because the instruments to express it do not exist.

Mercenary Capital and the Amnesia Machine

The absence of the time dimension does not create a neutral void. It creates a specific pathology: mercenary capital.

In a market where the longest available yield product expires in ninety days, rational behavior converges on a single strategy: maximize extraction within the current window, then move. This is not greed. It is optimization within the available structure. If the system offers no instrument to express a long-term view, then participants cannot hold long-term views — not because they lack the conviction, but because they lack the vehicle.

The behavioral pattern is now so consistent it has its own vocabulary. Incentive farming: enter a protocol the moment it launches a reward program, extract the subsidized yield, exit the moment the program expires. Liquidity mercenaries: provide liquidity only where incentives are richest, withdraw the moment a better opportunity appears. Bot-driven arbitrage: automated strategies that measure opportunity not in months or weeks, but in blocks — twelve-second increments on most chains.

The result is a liquidity landscape that resembles weather more than climate. Capital arrives in sudden storms and departs just as suddenly. A protocol can show $500 million in total value locked on Monday and $50 million on Friday — not because anything fundamental changed, but because an incentive program expired and the mercenaries moved to the next campaign. The numbers are real. The commitment behind them is fictional.

This is not a moral failure. It is a structural one. The participants are not behaving irrationally. They are behaving optimally within a system that has no instrument for time.

A market that cannot remember yesterday cannot commit to tomorrow. And a market that cannot commit to tomorrow cannot build anything that lasts.

Kahneman and Tversky identified the psychological mechanism: hyperbolic discounting. Humans systematically overweight immediate rewards relative to future ones. A dollar today feels worth more than $1.10 next year, even when the math says otherwise. This bias is hardwired — and it is massively amplified in an environment where the longest-dated instrument expires in three months.

But here is the part that nobody says out loud: DeFi did not merely inherit this bias. It monetized it. Traditional finance builds rigid structures — thirty-year bonds, penalty fees, lock-up periods — specifically to protect participants from their own temporal myopia. DeFi did the opposite. It built a multi-billion-dollar infrastructure optimized to weaponize impatience. The 90-day cycle is not a bug. It is an extraction architecture that feeds on the gap between what participants want now and what they need later. The mercenary farmer thinks he is playing the game. In reality, the game’s absence of duration is playing him. He is running on a ninety-day treadmill, mistaking speed for progress.

When every pool resets quarterly, every incentive expires monthly, and every strategy is measured in weeks, the entire market converges on the same temporal horizon. Long-term thinkers are not rewarded. They are punished — because the yields they forgo in the short term are captured by the mercenaries, and the stability they provide is not compensated by any structural premium. In traditional bond markets, duration is compensated: you earn a term premium for lending longer. In DeFi, duration is penalized: you earn less for staying put while the mercenaries hop.

Why This Matters Beyond DeFi

The absence of a yield curve is not a niche technical problem. It is the single greatest structural limitation preventing decentralized finance from becoming a serious financial system.

Institutional capital cannot operate in a market without time. Pension funds match assets to liabilities across decades. Corporate treasuries manage duration exposure across fiscal years. Sovereign wealth funds think in generational horizons. None of these actors can deploy capital into a system where the longest available maturity is ninety days. It is not a matter of risk appetite. It is a matter of structural impossibility. You cannot match a twenty-year liability with a three-month instrument, no matter how attractive the yield.

This is why, despite years of rhetoric about institutional adoption, the vast majority of institutional capital remains on the sideline of DeFi. The access problem has been solved. The custody problem has been solved. The regulatory landscape, while imperfect, is navigable. What has not been solved is the duration problem. And without duration, institutional deployment is not conservative — it is incoherent.

The consequence is that DeFi remains a retail-dominated, short-horizon, high-turnover market. This is sometimes celebrated as democratization. It is, in structural terms, a limitation. Retail capital is, by definition, small, impatient, and sentiment-driven. A market dominated exclusively by retail capital is a market that amplifies volatility, punishes patience, and rewards narrative over fundamentals. Not because retail participants are inferior — but because they operate under constraints that institutional capital does not share.

Every serious financial market in history has matured by extending its time horizon. Equity markets began as speculative day-trading venues and evolved into structures with forward earnings multiples, discounted cash flow models, and multi-decade institutional ownership. Bond markets began as short-term lending instruments and evolved into the most sophisticated duration-management infrastructure on the planet. Commodity markets began as spot trading and evolved into futures curves that extend years into the future.

DeFi has not made this transition. It remains stuck in the spot-trading phase — a perpetual now, without the instruments to extend into a structured future.

The Patience Asymmetry

The strongest counterargument first. DeFi’s short-term orientation is not a cognitive failure. It is a survival strategy.

In traditional finance, time is a measure of compounding. In decentralized finance, time is a measure of exposure. The longer your capital sits in a smart contract, the higher the cumulative probability that an exploit, a governance attack, or a protocol vulnerability erases it to zero. Hyperbolic discounting in DeFi is not merely a psychological artifact — it is a rational risk premium. Participants demand extreme yields on short lockups because they are implicitly pricing the possibility that the protocol will not exist on day ninety-one. You cannot build a ten-year yield curve on architecture that the market expects to be hacked next month.

This is real. Smart contract risk is the irreducible kernel of truth inside the 90-day casino. And any honest analysis must acknowledge it: the time dimension in DeFi carries a category of risk that does not exist in traditional finance. A Treasury bond may lose value. A smart contract can lose everything. The risk is not continuous. It is binary. And binary risk compounded over years is a genuine structural obstacle to long-duration deployment.

The second counterargument is less dramatic but equally honest: DeFi is simply young. Every immature market begins with short horizons. Equity markets were pure speculation before institutional capital demanded discounted cash flow analysis. Bond markets were short-term lending before governments needed to finance long-term obligations. The catalyst for maturation was always structural demand for longer duration — and DeFi has not yet experienced that catalyst at scale.

The third counterargument: perhaps DeFi does not need a yield curve at all. Perhaps a permanently short-horizon system serves a valuable function as a high-speed liquidity layer, and the duration problem should be solved elsewhere. DeFi excels as a spot-execution layer. But execution without time structure is trading, not finance. And trading alone cannot attract the capital that transforms a niche into infrastructure. A bond market without maturity structure is a money market fund. A financial system without a yield curve is a system that cannot price its own future.

Here is where the structural asymmetry emerges.

In a market where ninety-day thinking is the norm, the participant who operates on a longer horizon does not merely have an edge. They occupy a different game. They are not competing with the mercenaries for the same ninety-day yield. They are capturing value in a dimension the mercenaries cannot access — because the mercenaries’ instruments do not extend into that dimension.

This is not a metaphor. In any market, the premium paid to patience is inversely proportional to the supply of patience. When everyone is optimizing the same short window, the long end of the curve is structurally underpriced — because no one is competing there. The patient operator is not grinding against ten thousand bots for the same twelve-second arbitrage. They are the only bidder in a part of the market that the majority does not know exists.

In a casino, the house always wins. But in a 90-day casino, the participant who can think in years is not a gambler. They are the house.

Those who control a game’s rules design it to reward compliance within the existing time structure. The ninety-day cycle is not a law of nature. It is a constraint imposed by the available instruments. Change the instruments — extend the maturities, build the curve — and you change the game. The patient do not need the casino to reform. They need it to stay exactly as it is, while they operate on a different clock.

This is the structural edge that the Duration Thesis is built on: not a bet on any specific asset, but a bet on the dimension of time in a market that has systematically ignored it.

The Missing Map

DeFi has no memory.

It thinks in sprints, not cycles. It rewards speed, not conviction. It prices the present with extraordinary precision and the future not at all.

This is not a reason to dismiss it. It is a reason to understand where the greatest structural asymmetry of this decade is hiding.

To fix this, decentralized finance does not need faster chains, better interfaces, or higher token incentives. It needs the oldest, most powerful instrument in traditional finance. A map of time. A structure that allows capital to express a view beyond ninety days — unmasking mercenary capital for the short-term noise it is, and rewarding conviction with a premium the market currently cannot price.

It needs a yield curve.

The question is not whether DeFi will eventually build one. Every serious financial market in history has. The question is what it takes to build a curve that is real — not fictional, not subsidized, not propped up by token emissions that erode the very base they claim to reward. Duration is not a risk to be avoided. It is a product to be priced. And pricing it requires something the 90-day casino has never demanded: an asset with genuine economic gravity.

What exactly is a yield curve? Why is duration not a risk, but a product? And what happens when a permissionless system builds the one instrument that traditional finance assumed could never exist outside its walls? That is the subject of the next essay.

- J.

Author’s Note

My first book “The Proto-Postnational Age” covers the structural forces behind this thesis — why redistribution fails and ownership through protocols is the path forward.

My second book, “The Frame”, just dropped on March 1st. It goes deeper into how consensus systems, ledger theology, and the unbundling of the self reshape what we think of as governance, identity, and value. If this essay resonated, my books are the next level.

This essay contains no investment advice and names no specific assets. The structural argument is the point.